In our quest to find the best digital bank in the UK, we take a look at the top three. Monzo, Starling and Chase.

FCA data shows that nearly one in twelve of all personal current accounts are now with a digital bank such as Monzo or Starling.

Innovation, ease of use and customer service are some of the key reasons people are making the switch. And with the average person now likely to have friends, relatives or work colleagues using a digital bank, this trend is only going to increase. Is it time you switched to digital banking?

At the time of writing there are six digital banks in the UK, but not all of these offer personal current accounts. The big two are Monzo and Starling, but we’ll also include the newly formed Chase Bank in this guide as, although it doesn’t yet offer all of the features of its older counterparts, it is quickly coming up to speed.

Chase vs Monzo vs Starling – which digital bank should I choose?

I’ve spent time using all three accounts, right off the bat that I chose Starling as my daily account, with Monzo as a secondary account, and I stopped using Chase altogether.

Your use case might be different, and I not going to turn this into a Monzo vs Starling vs Chase debate, but instead run through a key list of personal banking features and see how each one performs, so you can decide which one best suits your needs.

Before we do that though, let’s get a brief overview of each of the challengers.

Starling bank overview

Despite the fanfare around Monzo, Starling was the first digital challenger to launch personal current accounts in the UK. It offers everything you need for day-to-day banking and continues to be a leader when it comes to innovative new features.

This innovation has seen Starling gain over 3m personal and business account customers since its launch in 2017.

Monzo – bank account overview

Monzo’s marketing success stems back to when it was pre-pay travel card. Since then, it has gone from strength to strength in terms of features, customer loyalty, and growth.

What Starling does quietly behind the scenes Monzo shouts about loud and proud, leading to it to be dubbed the ‘noisy neighbour’ (a term taken from the rivalry between Manchester United and Manchester City).

Fortunately for Monzo it backs up the marketing hype with one of the best accounts around, and until 2025, the largest subscriber base of any UK digital bank.

Tip: If you sign up for a Monzo bank account via our link you’ll get a free welcome bonus of between £10 and £50

Chase UK – bank account overview

Chase added itself to the Monzo vs Starling debate, when it launched its current account in winter 2021. It is the newest of the three main digital challenger banks. Don’t let that fool you though. It is backed by JP Morgan Chase the largest consumer bank in the US, and gained more than a million customers in its first 12 months. That’s more than Monzo and Starling managed together during their first year of operation.

What it offers over the other two is 1% cashback on spending (though this comes with some big caveats), 5% interest on ‘round-ups,’ and some of the most generous foreign ATM withdrawal limits around. Whether that is enough to attract and keep customers whilst the rest of the features are fleshed out remains to be seen.

See our full review of the Chase UK bank account here.

Opening an account a digital bank account with Monzo, Starling, and Chase

Opening an account with Starling, Monzo, or Chase is fast, free, and easy. The process is all done in app and requires that you take a photo of your ID, confirm your address, and take a short video selfie.

Account verification can take anything from a few minutes to a couple of hours, whilst your information is checked. In our tests it took a few attempts at uploading the ID to Chase, whereas the Starling and Monzo process was completed without hiccups. All accounts were open within an hour or less.

We’ve included links below should you want to open any of the three accounts:

>> Open a Starling bank current account

>> Open a Monzo current account

Monzo is currently offering a £10 -£50 sign up bonus. To get the bonus, simply sign up for a free Monzo account using the link above, and use your Monzo card within 30 days. The money will be deposited into your account immediate.

Does Monzo, Starling or Chase run credit checks?

It’s worth pointing out that although checks are made on your credit history these are soft searches and as such are not visible to other institutions and won’t affect your ability to obtain credit in the future. If you were rejected for one account, there is nothing to stop you applying at one of the other banks.

Paying in / out (cash and cheques)

Monzo and Starling both offer a switching service with seven-day switch guarantee. This allows you to move your account over to them complete with all of your direct debits, standing orders and payees.

Paying in cash over the counter

Paying in cash is probably the biggest area where traditional highstreet banks beat their digital counterparts. With the onset of contactless payments, and instant bank transfers cash use has been declining rapidly. For some users though cash is still king, so it’s important to be aware of the limitations of digital accounts in this area.

Starling account holders can pay in cash over the counter at 11,500 Post Office branches. This is fee free up £1000 per year. Anything over this incurs a 0.7% charge.

Monzo customers can pay in cash at 28,000 PayPoint locations across the UK. There is a maximum limit of £300 per transaction and £1000 per 180 days. Monzo passes on the £1 fee for this to the customer.

Chase doesn’t have any way for customers to pay cash into the account.

Winner: Starling

Paying in cheques

Yes, believe it or not cheques are still a thing. For a while it looked like they had died a death, but regulation changes to speed up the clearing process gave them something of a lifeline.

Starling users can pay in cheques valued at £1,000 or less via the Starling app. Cheques paid in this way can be drawn against the next working day. Cheques over £1,000, need to be posted to Starling, but there is a Freepost address you can use, so it doesn’t cost you anything.

To pay a cheque into a Monzo account you need to physically post it to Monzo, writing your account number on the back of the cheque. You can use Monzo’s freepost address but Monzo recommends it is sent via a tracked service.

The cheque itself takes Monzo 4-6 working days to process.

Again, Chase customers have no ability to deposit cheques.

Winner: Starling

International transfers

Starling customers can both send and receive international payments directly within the app. All costs and associated fees are presented upfront. With the option of sending a SWIFT payment at a slightly higher cost, or a low-cost payment which is roughly half the price, but doesn’t include proof of payment or personalised references.

A £1,000 SWIFT payment sent to a Eurozone country (as at 14/03/2022) will see the recipient receive €1,177.76

The same £1,000 payment sent via the low-cost method would see the recipient gain €1,183.95

Monzo is not connected to the SWIFT or SEPA network, and as such cannot reliably send and receive international payments itself. Instead, international transfers are handled by Wise.

A £1,000 payment sent to a Eurozone country will see the recipient getting €1,181.33

To put both of these into perspective. Send the same £1,000 to a euro account using Revolut, and the recipient would get €1,189.55

Chase hasn’t yet implemented sending or receiving international payments.

Winner: Starling

In credit Interest, benefits and incentives

Since its inception, Starling offered interest credit balances of up to £85,000. At one time it bumped that up to 3.25% before completely removing interest altogether.

Monzo has never offered an interest rate on in-credit balances on its free account, but it has introduced in-credit interest on its Plus and Premium accounts (see our review of Monzo premium).

Chase approached things differently. It doesn’t offer interest on in-credit balances, but instead offers 1% cashback on debit card spending for 12 months. In addition, it offers 5% AER on ‘round ups.’ Where spending on your account will be rounded up the nearest pound. And the rounded-up amount moved to separate ‘pot’ where it will earn 5% interest.

A similar program can be set up on Starling and Monzo accounts via integration with Moneybox where round-ups can be saved or invested.

Winner: Monzo

Savings account

All three banks now offer savings accounts, and as of August 2024 Monzo has taken the lead here. Where previously it offered savings accounts run by third parties. It now offers its own instant access savings account paying 2.75% AER.

As far as digital accounts go, this rate is only bettered by Kroo Bank, or Trading 212 (which of course isn’t a bank).

Chase allows its users to create up to 10 easy access savings accounts. Its easy access saver offers 2.25% AER.

Interest on both Chase and Monzo’s savings accounts is paid monthly, but Chase allows a maximum balance of £250,000. Bear in mind only the first £85,000 is protected, so if you have more than this, it would be best to spread it around different providers.

More recently, Starling announced a 1 year fixed savings account. The minimum balance starts at £2000, but your money is locked away for 12 months. After which you’d have earned £105 in interest on your £2,000. The maximum balance is £1,000,000. The interest rate as at September 2024 was 4.2% AER, but do be sure to check the starling website, as it changes regularly.

Winner: Monzo (just)

For more on savings see our overview of the best digital savings accounts

Budgeting

One area where Monzo has traditionally stood head and shoulders above others is in budgeting. Digital accounts have long featured payment categories, but Monzo’s approach to budgeting takes things a little further.

Users can track spending from payday to payday by selecting the last time they got paid in the app. This date can be changed at will as required.

There is also a monthly budget option where budgets can be set for each spending category e.g. entertainment, transport etc… As you spend the app will then tell you how close you are to these budget limits. It doesn’t stop you from overspending, but instead offers a gentle reminder to keep you on track.

The summary section of the app shows you what you’ve got left to spend in the current period taking into account money due in and out of the account in the future.

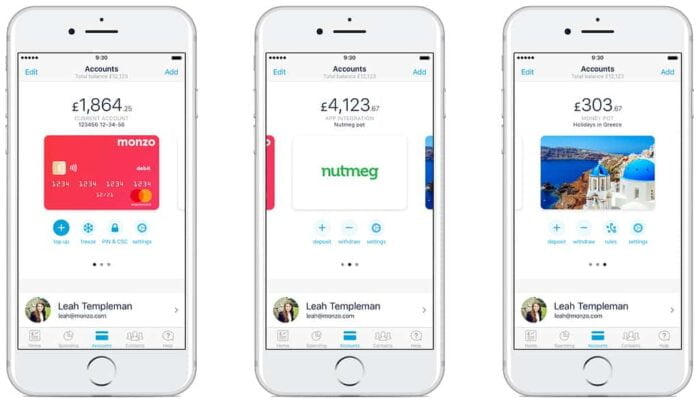

Finally, there’s Monzo’s Pots feature. Which is basically a way to set money aside outside of your main account balance. This is most commonly used for setting money aside for bills, and is one of the main reasons we’ve heard of people choosing Monzo over Starling.

Starling Bills Manager

Not to be outdone, Starling introduced its version of pots called spaces. In which you can find the Bills Manager. This actually goes one step further than Monzo’s pots by allowing you to pick a different space (as Starling calls it) to pay individual bills from.

This is a useful feature allowing you to keep things like subscriptions separate from household expenses.

Starling notifies you the day before a direct debit is due, and if you don’t have sufficient funds in that space it will let you know, so that you can make the transfer to the correct space.

Now with the Starling 1-year fixed savings account, you can also move money directly from savings spaces to your Starling savings account.

Multiple accounts with Chase

Chase is the least sophisticated of the three in this regard. Whilst it doesn’t have pots or spaces, it does allow you to add as many extra current accounts as you like. These can then be renamed and managed to meet your specific budgeting needs.

Each additional account comes with its own account number and sort code, and can be linked to your debit card for point-of-sale spending. The 2.7% savings account is also easy access, so you can withdraw or add funds to it as you please.

Winner: Monzo (still)

Overdrafts and borrowing

Monzo offers arranged overdrafts of up to £1,000 with a variable APR of 19%, 29% or a whopping 39%. It goes without saying the interest is high, so best to avoid these if possible.

Similarly, Monzo also offers unsecured loans between £7,000 up to £15,000. These start at an APR of 8.8% rising to 24%.

Starling offers overdrafts up to £1,200 with a variable APR ranging from 15%-35%. Helpfully it also provides an overdraft cost calculator and an eligibility checker so you can see how likely you are to be accepted before making an application and getting a hard search on your credit report.

There are also rumours that Starling is preparing to offer mortgages. It already manages a £2bn mortgage portfolio from its purchases of Fleet Mortgages and Masthaven last year, but reports suggest it will offer its own mortgage product in 2023.

Currently Chase does not offer any borrowing facilities at all.

Winner: Starling

Fees

Starling and Chase accounts are both free to open and use with no ATM or other hidden fees. Monzo is also free to open an account, but additionally it offers two subscription accounts too.

They are Monzo Plus, and Monzo Premium priced at £5 per month and £15 per month respectively. We won’t cover these here, but see our Monzo Premium account review for more information. The paid accounts come with a number of features and benefits over the free option. This can be to the detriment of regular account users though, as new features tend to get reserved for paid users.

Winner: Tie

Joint Accounts

Both Starling and Monzo offer joint accounts. It was actually one of the most requested features when the banks were launching. They each take the same approach in that in order to open a joint account both of you must first have current account with them.

This is quite different to a traditional bank where it’s possible to open a joint account without otherwise banking with that organisation. That being said, once you open your Monzo or Starling joint account, there is no requirement to actually use your personal accounts. These can just sit there dormant.

Bear in mind that in opening a joint account you will be financially linked to the other person on the account. Both account holders will have control of the money within the account. Legally anything in a joint account is owned 50/50 with the other account holder even if they haven’t contributed.

Chase doesn’t currently offer a joint account, but watch this space, as it’s likely to in the future.

Winner: Tie (Monzo/Starling)

Junior accounts

The Starling Kite account is an addon to a parents main account, and is aimed at children between 6-16 years old manage their pocket money. Parents have control and visibility over the account. Kids get a Kite card and access to their space on the Starling App. There’s a £2 a month fee for this.

Teens 16 and over can open their own Starling Teen account. This is a free account and comes will the features of a regular adult Starling account minus any borrowing.

Monzo doesn’t offer a kids account, but like Starling it does offer a teen account for those aged 16-17. Again, this is the same as the adult account but blocks spending to for some things which are illegal for under 18s e.g., Gambling websites, adult content sites etc…

Chase, being new to the market doesn’t currently offer any form of kids or teens account. That may change in the future though.

Winner: Starling

Travel

If you’re a frequent traveller then Chase is the winner here having recently wrestled Starling off the top spot.

All three offer fee-free foreign spending, so there won’t be any charges for using the card abroad, or on foreign websites. They all also benefit from the Mastercard exchange rate meaning you’re getting the best rate possible when spending in foreign currencies, with zero loading or commission.

Where Chase starts to pull ahead is in ATM withdrawals. Chase has a £1,500 monthly limit on fee free foreign currency withdrawals. Although that doesn’t beat Starling’s limit which is effectively £9,000.

Chase has a higher daily maximum limit of £500 equivalent vs. £300 for Starling. Monzo limits free foreign withdrawals to just £400 a month (up from £200 in 2023).

In addition, Chase customers can also use Chase Bank ATMs in the United States without incurring any charges. Typically, ATMs in the US charge between $3-8 for withdrawals unless you’re withdrawing from the same bank that issued your card.

For more on travel see our guide to the best travel debit and credit cards for foreign travel

Winner: Chase (just)

Customer service

Another area where digital banks race ahead of their traditional counterparts is in customer satisfaction. Whilst First Direct was always top a choice when it came to customer service and satisfaction, it didn’t take long for new crop of challengers to race ahead.

Monzo comes out ahead of starling by 2 percentage points in the FCA satisfaction survey in 2021. Though Starling has won the Best British Bank Account Awards for four years in a row.

Having launched its digital account in late 2021, there isn’t as much data on Chase’s customer service as the other two banks. That being said, so far it scores a 4.2 out of 5 on Trustpilot.

Winner: Monzo

Monzo vs Starling vs Chase – Which one is best?

It’s easy to see how all three banks are similar. Chase has the slight disadvantage of being a new entrant to the market, but it’s backed by one of the largest financial institutions in the world. Until recently, it was something of a coin toss between Monzo and Starling. Monzo had the better budgeting features, but Starling was better for using abroad.

Now we’re starting to see some clear daylight between the two as they go about their businesses in different ways. Starling continues to bring new features to its account (e.g. virtual cards) whereas Monzo reserves these for paying customers only.

Chase is the most rewarding account with it’s 1% cashback and high interest easy access saver, but the former is only for the first 12 months (we expect a new offer sooner or later), and the latter is beaten by Monzo and Kroo.

Overall it’s Starling that appears to the one offering the most complete service i.e. most or all of the services you might expect from a traditional high street bank, and with a mortgages product on the way, its the one I personally use the most.

Ownership

These days social and political pressures mean ownership transparency is more important than ever. In personal banking it carries an added importance as FSCS payments are limited on a per institution basis rather than per account.

Fortunately, there is nothing to worry about here with these digital accounts.

Who owns Monzo?

Monzo was founded in 2015 by Tom Blomfield and others. Tom and his team actually met whilst working for Starling, before a disagreement with Starling founder Anne Borden saw him leave to setup Monzo. Tom has since left the bank.

Despite its popularity, Monzo is yet to make a profit. That is fair enough, as these things take time, but what’s worrying is that its losses have been growing substantially. In fact, Auditors Ernst & Young voiced their doubts about the bank as a going concern.

Fortunately, with full FSCS protection that’s not something customers really need to worry about, and Monzo is such hot property it would likely be bought out or be able to bring in new investment if needed.

Who owns Starling Bank?

Starling is a privately owned bank founded by CEO Anne Boden (former COO of Allied Irish Bank) in 2014. Anne owns roughly 24% of the bank with the rest being made up of private investors. Starling is not part of any other banking group.

In 2020 there were reports that larger banks were looking at acquiring Starling, but Anne dismissed these claims and aims to take Starling public in 2022.

Who owns Chase?

Unlike the other two challengers which were new start-ups when they launched, Chase is owned by JP Morgan Chase, which is not only the largest banking providers in the US with over 50 million customers, but one of the largest banks in the world. JP Morgan is involved in all aspects of banking, and particularly investment banking.

Business banking

We’ve put this at the bottom, as it’s not relevant for the vast majority of banking customers. Would-be entrepreneurs, or those with side hustles, small businesses, or taking occasional freelance work, may be interested in opening a business bank account in the future. While this doesn’t have to be with same bank you hold a current account with, it can help speed up the process.

Chase in the UK is purely focused on personal current accounts. As of yet there haven’t been any rumblings about offering business bank accounts. It still has some way to go to polish its personal accounts first.

Both Mozo and Starling offer business bank accounts for sole traders and limited companies. Starling has the slight edge over Monzo here, but there isn’t much in it. See our long term review of Starling Business banking here.

Just as with current accounts, always have more than one business bank account, as a back up. Both the Starling and Monzo Business accounts are free to open, so there’s nothing stopping you opening an account with each of them. Alternatively, specialist business account providers such as Tide could be worth a look as a backup.

For more on business banking see our business bank account guide.

Digital banking FAQs

Do digital bank accounts run credit checks?

Chase, Mozo and Starling all perform soft searches of your credit history report when applying for the account. A soft search isn’t normally visible to other lenders, which means if you aren’t accepted, it shouldn’t prevent you from applying elsewhere.

The searches performed by the three UK digital banks are mainly for fraud and identification purposes rather than credit worthiness.

As a note though, Starling and Monzo do offer overdraft facilities (applied for separately). If you apply to take out an overdraft, a hard search will be carried out, and it will be visible to other lenders.

It is often recommended to leave at least 3 months after a hard search before applying any further credit or big-ticket items such as mortgages.

Is digital banking secure?

One of the joys of digital banking, is not having to typing in various usernames, passcodes, passwords etc. or using one of those terrible card readers for adding and amending payees (Yes Nationwide I’m looking at you).

That doesn’t mean digital accounts aren’t secure. Many the likes of Monzo and Starling in particular have built their platforms from the ground up with security in place to ensure that fraudsters can’t hack into your account, but that doesn’t mean you don’t have to take the normal precautions.

Additionally, digital banks were ahead of the curve when it came security, allowing customers to turn off their cards for various types of purchase, use geofencing, and prevent ATM withdrawals. These days many traditional banks have followed that model within their apps, but digital banks still lead the way when it comes to empowering customers to manage their security.

Is my money protected in a digital bank?

Chase, Monzo and Starling are all fully regulated UK banks, and so are covered by the FSCS. That means your money up to the tune of £85,000 is protected in same way it would be with any of the big-name high-street banks. If you are in doubt you can check if your institution is covered with the FSCS bank and savings protection checker.

Have you gone digital yet? Tell us what you love about your digital bank in the comments below